In addition to understanding what financing options exist to help customers pay for a solar installation (as discussed in the previous article in this series), it is important to understand how these options compare side by side. In this article, we walk you through some important considerations to bear in mind when evaluating the various financing options.

The chart in Figure 1 below may be a helpful reference when evaluating which financing method best fits the situation and priorities of a prospective solar customer. The considerations illustrated in the chart are discussed in greater detail below.

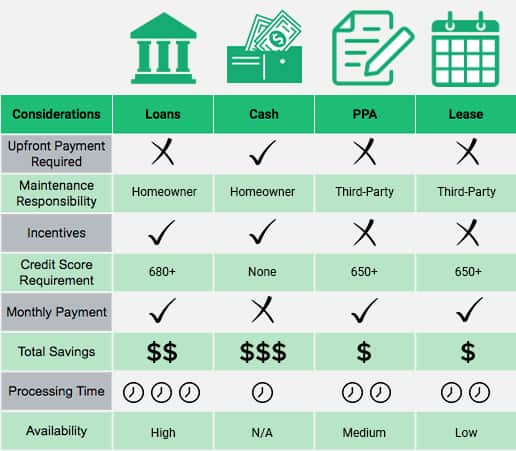

Figure 1. A comparison of the differences between the four most common solar financing options. Note that these considerations are presented from the perspective of the homeowner (for instance, incentives for systems financed with a lease or loan may be available to the third-party system owner, but typically would not be available to the homeowner.)

Figure 1. A comparison of the differences between the four most common solar financing options. Note that these considerations are presented from the perspective of the homeowner (for instance, incentives for systems financed with a lease or loan may be available to the third-party system owner, but typically would not be available to the homeowner.)

Upfront Payment Requirements

Solar loans, PPAs, and leases often allow homeowners to install solar with little to no payment upfront. However, should the homeowner decide to pay a small portion of the cost upfront, it may be possible for them to obtain more favorable terms and interest rates for their loan or lease. With cash financing, the entire cost of the system is paid upfront.

Maintenance Responsibility

Generally, solar installations require very little maintenance, as solar panels are durable and weather-resistant. Nonetheless, if a homeowner finances their system with cash or a loan, they are responsible for any maintenance should the installation be damaged. This is not the case for the majority of PPAs and leases, in which the third-party provider is responsible for maintenance or repairs. However, in some of these agreements, the homeowner may still be responsible for specific maintenance costs like inverter replacement.

Incentives

Homeowners that finance their solar installation with loans or cash are eligible for several federal, state, and local incentives for going solar (discussed in greater detail in Part 4 of this series, Financial Incentives for Installing Solar), such as the federal Investment Tax Credit, which allows system owners to deduct 30% of the cost of the solar installation from the amount they owe in federal taxes. These incentives apply only to the owner of the installation and thus are not available to customers who finance their installations with leases or PPAs.

Credit Score Requirement

While there is obviously no credit score requirement when paying for a solar installation in cash, a credit score within a certain range may be necessary to qualify for loans, leases, and PPAs. Generally, a FICO credit score in the high 600s (out of 850) gives a borrower a good chance of being accepted for these financing options. For those with a lower credit score, some states offer special loans or financing options, including on-bill financing, which attaches the payment of the loan to the borrower’s electric bill.

Monthly Payment Considerations

One benefit of paying for a solar installation upfront with cash is the absence of monthly payments. From day one, 100% of the energy produced by the system is free for the homeowner, no strings attached. This is not the case for loans, leases, and PPAs.

With loan financing, minimum monthly payments are required to pay off the solar loan. While this monthly minimum payment is often fixed, homeowners can choose to pay more than the minimum in order to pay off the loan sooner and reduce what they pay in interest charges. Like loans, solar leases have predetermined, fixed monthly charges; these charges continue for the duration of the contract. Depending on the agreement, the homeowner may have the opportunity to purchase their solar installation at some point during the lease or after it expires.

Unlike the fixed monthly payments of loans and leases, the monthly charge under a PPA will depend on the number of kWh the installation produces over the month. Although these financing options all require monthly payments, the amount paid per month will typically be less than what the homeowner currently pays for electricity, allowing the homeowner to see savings immediately.

Total Savings

A customer’s total savings over the lifetime of their solar installation depend on many factors, including how utility rates change over time and, for solar loans, their interest rate. However, as discussed in Part 2 of this series Your Solar Finance Primer, typically cash financing maximizes lifetime savings compared to solar loans, leases, and PPAs, as customers avoid interest charges and monthly payments while gaining access to free electricity produced by their installation.

Similarly, the total savings from a loan will likely be greater than from leases or PPAs, because homeowners benefit from free energy produced by their system after the loan is paid off. With leases and PPAs, homeowners are required to pay monthly for the entire term of the agreement. However, these options can still make financial sense because the payment is typically lower than what the customer would pay for the same amount of energy from their utility.

Processing Time

Solar leases and PPAs are typically processed quickly, often in a single meeting with the third-party financier. Solar loans, on the other hand, generally take several weeks to be approved as they involve additional financial evaluation to determine a homeowner’s creditworthiness and the interest rate the financing institution is willing to offer. Because there is no borrowing involved in cash financing, processing time is avoided entirely.

Availability

While loans are widely available from banks and solar lending institutions, PPAs and leases are less common. Only 26 states have clearly authorized the use of PPAs, and the legality of leases also varies across the country. Obviously, the availability of cash depends on individual circumstance. As addressed above, credit score can also affect the accessibility of some financing options, especially for those with scores below 650.

~~~

We hope that this discussion of the differences between financing options will help you guide your customers toward an understanding of which financing option will best meet their needs!

For those interested in a deeper exploration of solar financing options, here are some additional resources you may find helpful:

- A Homeowner’s Guide to Solar Financing by the Clean Energy States Alliance (CESA)

- Solar Leasing for Residential Photovoltaic Systems by the National Renewable Energy Laboratory (NREL)

- Homeowners Guide to Financing a Grid-Connected Solar Electric System by the U.S. Department of Energy (DOE)

About Solar Finance 101

Evaluating Solar Financing Options: Factors for Your Customer to Consider is Part 3 of Solar Finance 101, a five-article series that serves as an introductory primer on the financial considerations of solar installations:

Article 1: How Solar Customers Save Money: A Beginner’s Guide to Net Energy Metering

Article 2: Your Solar Finance Primer: What to Know About the Top Four Solar Financing Options

Article 3: Evaluating Solar Financing Options: Factors for Your Customer to Consider

Article 4: Financial Incentives for Installing Solar: A Beginner’s Guide

Article 5: Quantifying Value of a Solar Installation: Some Helpful Metrics